Standing at a rental car counter after a tiring flight is a universally stressful experience. Then he gives you a clipboard and draws your attention to a scary-looking list of acronyms such as CDW, LDW, and SLI and tells you that for $30 more per day, you can save yourself from losing everything financially. Panic strikes you instantly. Nobody wants to pay for a destroyed vehicle, but the cost of double the daily rental rate for insurance is hard to bear.

In order to make an informed decision without overspending on it, you will have to know how the rental car insurance works, what coverage you already have, and what additional coverage you need.

Decoding the Rental Counter Menu

When you arrange a car rental with airport pickup in Dubai or anywhere else globally, the rental agency will present you with four primary insurance options. They are packaged as individual add-ons, but they essentially cover two things: damage to the vehicle and liability for everyone else.

1. Collision Damage Waiver (CDW) / Loss Damage Waiver (LDW)

Strictly speaking, this is not actual insurance. It is a waiver where the rental company agrees not to sue you if the car is damaged, stolen, or vandalized while in your possession.

- What it covers: Bodywork, frame damage, and theft of the vehicle. It also usually covers “Loss of Use” fees, which are the charges an agency levies for the revenue they lose while the car is sitting in a repair shop.

- The catch: It typically comes with a deductible (excess) unless you pay for a “zero-deductible” upgrade.

2. Supplemental Liability Insurance (SLI)

If you hit another vehicle, a pedestrian, or someone’s property, you are legally liable for the damages. SLI steps in to cover those costs up to a specific limit, usually around $1 million. Most countries require rental agencies to carry a bare-minimum level of liability by law, but this basic coverage is easily exhausted in a serious accident. SLI provides the necessary cushion.

3. Personal Accident Insurance (PAI)

PAI covers medical costs for you and your passengers if you are injured in an accident while driving the rental car. It also includes a small accidental death benefit.

4. Personal Effects Coverage (PEC)

This will safeguard your material possessions (computers, suitcases, clothes) if they get stolen from within the car. This coverage is normally limited to a lower maximum amount for each item and a total sum for each occurrence.

Along with securing the right insurance, following essential road safety tips—such as locking the vehicle, parking in well-lit areas, and never leaving valuables in plain sight—can significantly reduce the risk of theft and help protect your belongings throughout your journey.

The Hidden Safety Nets: What You Already Own

Before you blindly agree to everything at the counter, you should review your existing assets. Most drivers carry duplicate coverage through two main avenues: their personal auto insurance and their credit cards.

+—————————+———————————–+———————————–+

| Coverage Type | Personal Auto Policy | Premium Credit Card |

+—————————+———————————–+———————————–+

| Damage to Rental Car | Yes (Matches your collision/comp) | Yes (Often secondary; primary on |

| | | high-tier cards) |

+—————————+———————————–+———————————–+

| Injury to Others | Yes (Matches your liability limits) | No |

+—————————+———————————–+———————————–+

| Stolen Personal Property | No (Often covered by homeowners/ | Rarely (Check specific baggage |

| | renters insurance) | benefits) |

+—————————+———————————–+———————————–+

Your Personal Auto Policy

However, since you have an auto insurance policy that covers the comprehensive and collision aspects, most likely the same coverage will apply to your rental car in your home country. In case your personal insurance policy carries a deductible of $500 for the comprehensive and collision coverage, then even in case you have an accident in the rental car, the deductible of $500 will apply.

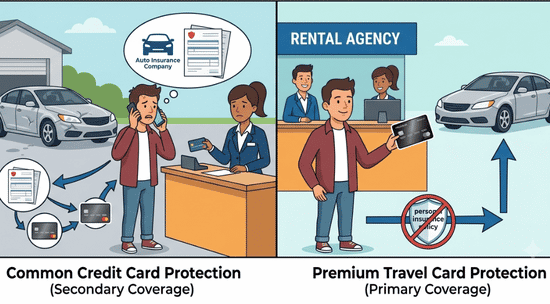

Your Credit Card Protection

Many rewards credit cards offer built-in rental car protection, provided you decline the rental company’s CDW/LDW and charge the entire rental amount to that specific card.

However, you must know the difference between primary and secondary coverage:

- Secondary Coverage: This is the most common type. If you crash the car, you must file a claim with your personal auto insurance first. Your credit card will only step in to pay whatever your auto policy misses, such as your deductible or administrative fees.

- Primary Coverage: Available on premium travel cards, this protection takes center stage. It pays out directly to the rental agency, meaning you completely bypass your personal insurance company, sparing you from potential premium hikes.

When Should You Actually Buy the Counter Insurance?

Despite having alternative options, there are distinct scenarios where paying for the rental company’s coverage is the smart, stress-free move.

- International Travel: Your domestic personal auto insurance almost certainly stops at international borders. While credit cards may still offer CDW protection globally, third-party liability is rarely provided by cards. In many overseas destinations, purchasing the local liability and CDW protection is highly recommended to comply with regional legal systems.

- You Don’t Own a Car: If you do not have a personal auto policy and your credit card only offers secondary coverage, you have no baseline protection. You must buy the counter coverage to ensure you are legally protected.

- You Want Zero Hassle: Filing an insurance claim through your personal policy or a credit card provider involves mountains of paperwork, waiting weeks for reimbursement, and the risk of rising premium rates. Buying the counter CDW allows you to simply hand over the keys after an accident and walk away completely clear of liability.

Final Strategy: Navigating the Counter

To protect your wallet, do your homework 24 hours before your trip. Call your auto insurance provider to confirm your exact coverage limits on rentals, and review your credit card’s guide to benefits.

This preparation becomes even more vital when handling specialty vehicles. Standard policies and credit cards explicitly exclude exotic cars, vans, or trucks due to their extreme value.

If you are eyeing the breathtaking supercars available for rent in Dubai or planning a luxury track experience, you will need to secure specialized commercial coverage or buy directly from the provider’s premium tier. By knowing exactly what your existing policies protect before you arrive, you can confidently tell the agent “no thank you” to the fluff, and only purchase the precise coverage you actually need.